7(a) Working Capital Pilot program

If you run a small business and you’ve ever struggled with cash flow gaps, slow-paying clients, or the cost of stocking up inventory before a big order you already know how painful it is to operate without reliable access to working capital. The 7(a) Working Capital Pilot program was built specifically to fix that problem. It’s one of the most flexible, affordable, and forward-thinking financing tools the SBA has ever launched for small businesses.

This guide breaks down everything you need to know from eligibility and loan terms to how you can actually apply and start using this facility to grow your business.

What Is the 7(a) Working Capital Pilot Program?

The 7(a) Working Capital Pilot program is a monitored line of credit offered through the SBA’s existing 7(a) loan program. Think of it as a smarter, more flexible version of a traditional business line of credit backed by the federal government and designed with the real needs of modern small businesses in mind.

Unlike a standard term loan where you receive a lump sum and start paying interest immediately, a line of credit only charges interest when you actually draw on the funds. That means you’re not bleeding money on idle capital. It’s a much more efficient way to manage your operating capital and that’s exactly why the SBA designed the WCP around this structure.

Overview of the 7(a) WCP by the U.S. Small Business Administration

The U.S. Small Business Administration officially launched the 7(a) Working Capital Pilot program with one clear goal: to serve as SBA’s premier working capital program. It combines the best features of SBA’s existing permanent 7(a) line of credit delivery methods into a single, unified facility that growing businesses can actually use.

What makes this program stand out isn’t just the government backing it’s the innovation baked into its design. The WCP introduces a new annual fee structure, support for both transaction-based and asset-based lending, and the ability to cover both domestic and international orders under one loan. The SBA also added one-on-one counseling through Finance Managers so lenders and borrowers aren’t navigating this alone. It’s a program clearly built by people who actually talked to small business owners first.

Key Benefits of the 7(a) Working Capital Pilot Program

The biggest advantage of the 7(a) Working Capital Pilot program is its flexibility. You only pay for what you use. Interest accrues only when you draw funds so if your line sits untouched for two months, you’re not paying for those two months. That kind of efficiency is a game-changer for businesses with seasonal revenue or irregular cash flow cycles.

Beyond the interest structure, this program opens doors that traditional financing just doesn’t. It supports transaction-based lending, meaning you can access funds earlier in your sales cycle before an invoice is even paid. It also supports asset-based lending so you can borrow against accounts receivable and inventory you already own. And if you’re thinking about expanding internationally, the WCP lets you finance both domestic and export orders under a single facility. No need to juggle two separate loans.

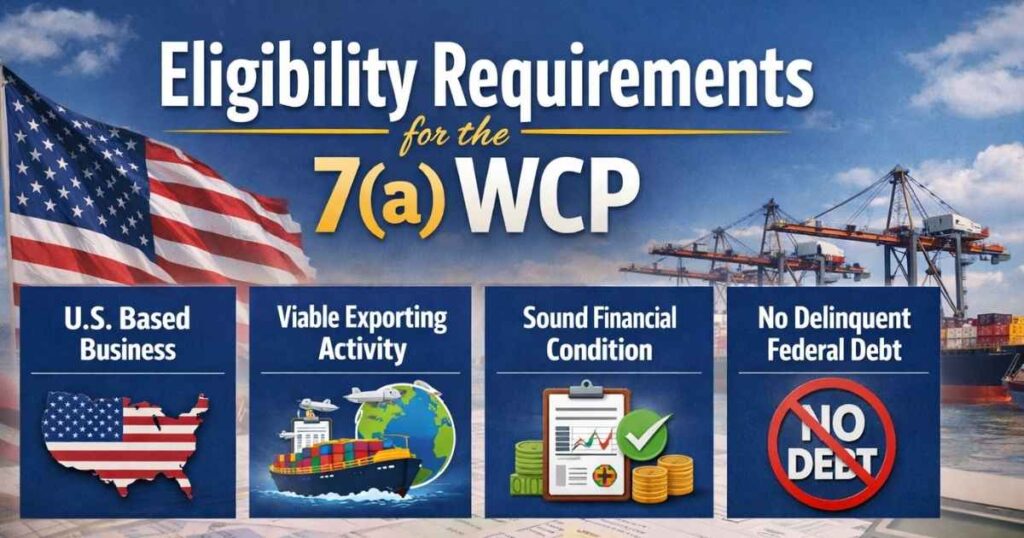

Eligibility Requirements for the 7(a) WCP

Not every business qualifies and it’s worth knowing the requirements upfront before you invest time applying. The core eligibility rules follow SBA’s standard SOP 50 10, Section A guidelines but the WCP adds a few specific requirements on top of those.

First, your business must have at least 12 full months of operating history before you file an application. Startups, unfortunately, don’t qualify for this one. If you’re applying to finance an acquisition, the acquiring business still needs that 12-month track record. Second, you must be able to produce accurate, timely financial statements including accounts receivable and accounts payable agings and inventory reports. The SBA needs to monitor your working capital activity and that requires real, reliable data on a regular basis.

How to Participate in the 7(a) Working Capital Pilot Program

If you’re a lender already approved to process 7(a) loans, you could start processing WCP loans as of August 1, 2024. Lenders who already hold delegated EWCP authority were automatically granted delegated authority to make WCP loans no extra steps needed. If you don’t have that authority yet, you can still apply for delegated 7(a) WCP status by following the requirements outlined in the Program Guide.

For small business owners, the path is through an approved lender. The SBA encourages both lenders and borrowers to reach out to local Finance Managers for guidance even on domestic transactions. These are subject-matter experts who know this program inside and out. Don’t try to figure it all out on your own when free expert support is literally part of the program.

Loan Terms, Limits, and Interest Rates

Here’s where things get concrete. The WCP offers a maximum loan size of $5,000,000 which covers the needs of most growing small businesses. The SBA guaranty percentage is 85% for loans up to $150,000 and drops to 75% for loans above that threshold. Loan maturity goes up to 60 months, giving you a solid five-year window to manage your working capital needs.

Interest rates are capped based on loan size, keeping borrowing costs reasonable across the board. Here’s a quick breakdown:

| Loan Amount | Maximum Interest Rate |

| $50,000 or less | Base rate + 6.5% |

| $50,001 – $250,000 | Base rate + 6.0% |

| $250,001 – $350,000 | Base rate + 4.5% |

| $350,001 and above | Base rate + 3.0% |

The larger your loan, the lower the spread above base rate. That’s a smart structure for businesses scaling up their working capital needs over time.

New Annual Fee Structure Explained

One of the most borrower-friendly features of the WCP is its annual fee structure, which is modeled after the SBA’s Export Working Capital Program. Instead of paying a flat, upfront guaranty fee based on the full loan amount, borrowers pay a short-term annual fee that’s proportional to how long they actually use the facility.

This means if you only need the line of credit for six months instead of a full year, your fee reflects that. You’re not being charged for time you don’t use. It’s a smarter, fairer way to structure fees and it gives small businesses real control over their financing costs. Customization is the key word here the WCP lets you shape the facility around your actual needs, not the other way around.

Support for Transaction-Based Lending

Traditional lines of credit typically release funds only after you’ve delivered goods or completed services. Transaction-based lending flips that model on its head. Under the WCP, you can access working capital at an earlier point in your project cycle before the work is fully done or the invoice is paid.

This is especially valuable for businesses that take on large contracts or projects with long lead times. Imagine winning a $500,000 contract but needing $150,000 upfront to cover materials and labor. Transaction-based lending through the WCP means you don’t have to turn down that opportunity because of a cash flow gap. You can move forward with confidence and cover all related costs from start to finish.

Support for Asset-Based Lending

Asset-based lending is one of the most practical and underused tools in small business finance. The WCP makes it more accessible by allowing you to borrow directly against the value of your accounts receivable and inventory. If your business has solid assets tied up in unpaid invoices or stocked shelves, this program helps you unlock that value without waiting.

For businesses currently using SBA Express loans, the WCP also offers a natural upgrade path. You can transition into a larger, more robust commercial working capital facility that better supports your growth trajectory. It’s not just a loan it’s a structural upgrade for how your business manages and leverages its financial assets day to day.

Export Finance Opportunities Under the WCP

Thinking about going global? The WCP has you covered. One of its most unique features is the ability to provide working capital against both domestic and international orders under a single loan facility. You don’t need a separate export line of credit to start selling overseas.

This is a huge deal for new-to-export firms. Historically, small businesses interested in international markets faced a confusing maze of financing options, separate applications, and added paperwork. The WCP simplifies all of that. You can open up international markets using the same facility you’re already using for domestic operations. It lowers the barrier to entry and makes global expansion a realistic option for small businesses that are just getting started with exports.

Eligible Lenders and Delegated Loan Processing

Not every bank or credit union participates in the WCP and that matters when you’re choosing where to apply. Eligible lenders are those already approved to process SBA 7(a) loans. Within that group, lenders with existing delegated EWCP authority automatically qualify for WCP delegated authority as well.

Lenders who want delegated processing status but don’t yet hold EWCP authority can apply through the process outlined in the Program Guide. The SBA’s Preferred Lender Program plays a big role here PLP lenders can process WCP loans faster because of their existing delegated authority. If speed is a priority for your business, working with a PLP-approved lender is the smart move.

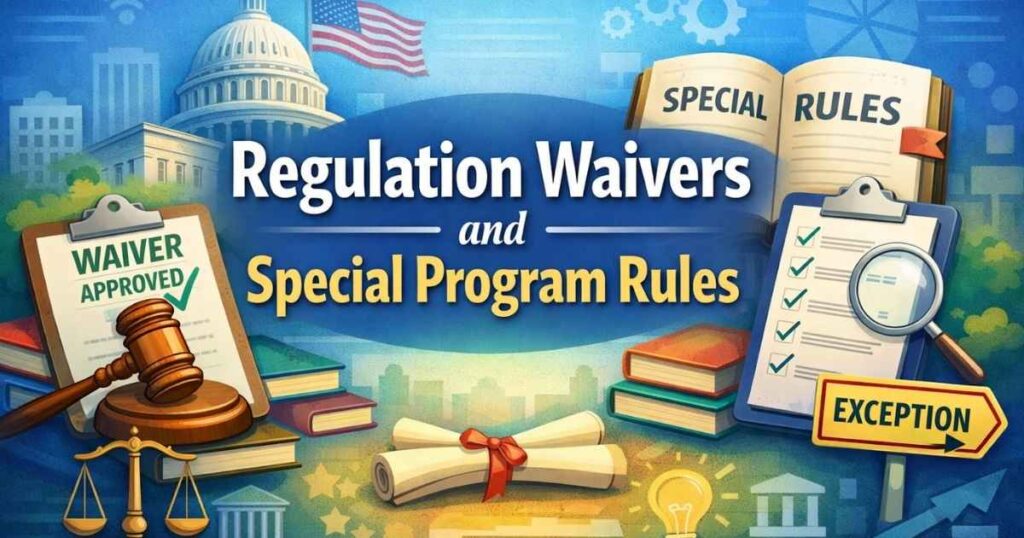

Regulation Waivers and Special Program Rules

Because the WCP is a pilot program, the SBA has built in some regulatory flexibility to allow it to test innovative features that don’t exist in permanent 7(a) loan products. Certain standard 7(a) rules have been waived or modified to accommodate the WCP’s unique structure particularly around monitoring requirements, fee structures, and transaction-based draw mechanics.

These waivers aren’t loopholes they’re intentional design choices that allow the program to function as intended. The SBA modeled much of the WCP’s framework after the Export Working Capital Program, which has a long track record of success. That said, lenders are expected to maintain strong operational controls that meet industry standards for asset-based facilities. The flexibility is there but so is the accountability.

Budget Impact on the 7(a) Loan Program

Any new SBA program raises a fair question: what does this cost taxpayers? The WCP was designed with fiscal responsibility in mind. Its annual fee structure rather than a one-time upfront guaranty fee creates a more predictable revenue stream for the SBA’s loan guaranty program over time.

The SBA also structured the WCP to operate within the existing 7(a) loan program budget framework, minimizing the need for additional appropriations. Because it’s a pilot program, it gives the SBA an opportunity to evaluate the real-world budget impact before deciding whether to make it permanent. The goal is to expand access to small business funding solutions without putting undue strain on the government-backed loan guaranty system.

Program Guide, SBA Notices, and Training Resources

If you want to go deeper, the SBA publishes a full Program Guide specifically for the WCP. It covers everything from lender eligibility and delegated authority requirements to detailed guidance on transaction-based and asset-based lending mechanics. This is the primary reference document for lenders who want to participate.

In addition to the Program Guide, the SBA issues official notices and updates as the program evolves. Lenders and business owners should also take advantage of the one-on-one counseling available through SBA Finance Managers. These sessions are free and tailored to your specific transaction whether it’s a domestic working capital need or a cross-border export deal. Training resources are available through SBA district offices and online channels, making it easier than ever to get up to speed quickly.

Program Evaluation and Future Outlook

The WCP launched as a pilot for a reason the SBA wants to see how it performs in the real world before committing to it permanently. The agency will evaluate program uptake, default rates, borrower outcomes, and lender participation to determine whether the WCP should become a permanent feature of the 7(a) loan program.

Early indicators suggest strong demand. Small businesses across industries have been looking for exactly this kind of flexible, monitored line of credit backed by a government guaranty. If the program meets its performance benchmarks, there’s every reason to expect it will evolve into a permanent small business funding solution. For now, it’s one of the most exciting and practical government programs for business cash flow support that the SBA has introduced in years and you’d be wise to explore it while it’s available.

FAQ’s

What is the maximum loan amount under the 7(a) Working Capital Pilot program?

The maximum loan size is $5,000,000, with SBA guaranty coverage of 85% for loans up to $150,000 and 75% for loans above that amount.

Can startups apply for the 7(a) WCP?

No. The program requires at least 12 full months of business operations before an application can be filed. It’s designed for established businesses, not startups.

How is the WCP different from an SBA Express loan?

The WCP offers a larger, more structured working capital facility with asset-based and transaction-based lending features that SBA Express doesn’t support. It’s built for businesses that have outgrown Express-level financing.

What interest rates apply to the 7(a) Working Capital Pilot program?

Rates are capped based on loan size, ranging from base rate + 6.5% for loans of $50,000 or less down to base rate + 3.0% for loans above $350,000.

How do I find a lender that participates in the WCP?

Start with SBA-approved 7(a) lenders, particularly those in the Preferred Lender Program. You can also contact your local SBA district office or Finance Manager for a referral to a participating lender near you.

Conclusion

The 7(a) Working Capital Pilot program isn’t just another government loan it’s a genuine rethink of how small businesses should access working capital. From its flexible annual fee structure and transaction-based lending support to its asset-backed borrowing options and export financing features, it addresses the real, everyday challenges that small business owners face. It’s practical, well-designed, and backed by the full weight of the SBA’s loan guaranty program.

If your business has been operating for at least a year and you need a smarter way to manage cash flow, fund growth, or take on bigger opportunities this program deserves a serious look. Talk to an approved SBA lender, connect with a Finance Manager, and find out whether the WCP is the right fit for where your business is headed. The tools are there. It’s up to you to use them.

Olivia Grant is a business strategist and content marketer with over a decade of experience helping startups grow online. He specializes in brand storytelling, SEO, and digital growth strategies. His insights blend practical experience with data-driven results, empowering entrepreneurs to build visibility and authority in competitive markets.